Thursday, July 4, 2024 06:14 PM

Pakistan's Tax Laws Amendment Bill 2024: Key Changes Revealed

- Reduced time frame for filing appeals in high courts to one month

- Abolition of commissioner appeals forum to simplify legal platforms

- Proposed increase in cost of seeking justice for individuals and companies

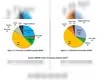

Image Credits: Business Recorder

Image Credits: Business RecorderThe proposed Tax Laws Amendment Bill 2024 in Pakistan aims to expedite tax dispute resolution, enhance transparency, and improve revenue collection mechanisms by introducing key changes such as reducing appeal time frames and simplifying legal platforms.

The federal cabinet has given initial approval to amend Pakistan's tax laws, aiming to streamline the tax dispute resolution process and enhance revenue collection efficiency. The proposed Tax Laws Amendment Bill 2024 includes significant changes such as reducing the time frame for filing appeals against tax cases in high courts to just one month, from the current three months. High courts will be mandated to decide tax-related cases within six months, with only special benches designated to hear such matters.

One of the key amendments is the abolition of the commissioner appeals forum, simplifying the legal platforms available to taxpayers. The bill also suggests increasing the cost of seeking justice by 150% for individuals and 300% for companies. Additionally, the limit for disputed tax amounts eligible for resolution through the Alternate Dispute Resolution Committee (ADRC) is proposed to be halved to Rs50 million.

Furthermore, the bill aims to strengthen the appellate tribunals by appointing experienced legal professionals and setting up a new directorate general of law. It also proposes the deletion of certain sections in the Sales Tax Act to streamline the appeals process and transfer pending cases to the appellate tribunals.

Overall, these amendments seek to expedite tax dispute resolution, enhance transparency, and improve revenue collection mechanisms. While some concerns have been raised regarding the implications on taxpayers, particularly companies, the government emphasizes the need for efficient tax administration to recover outstanding revenues and ensure compliance with tax laws.